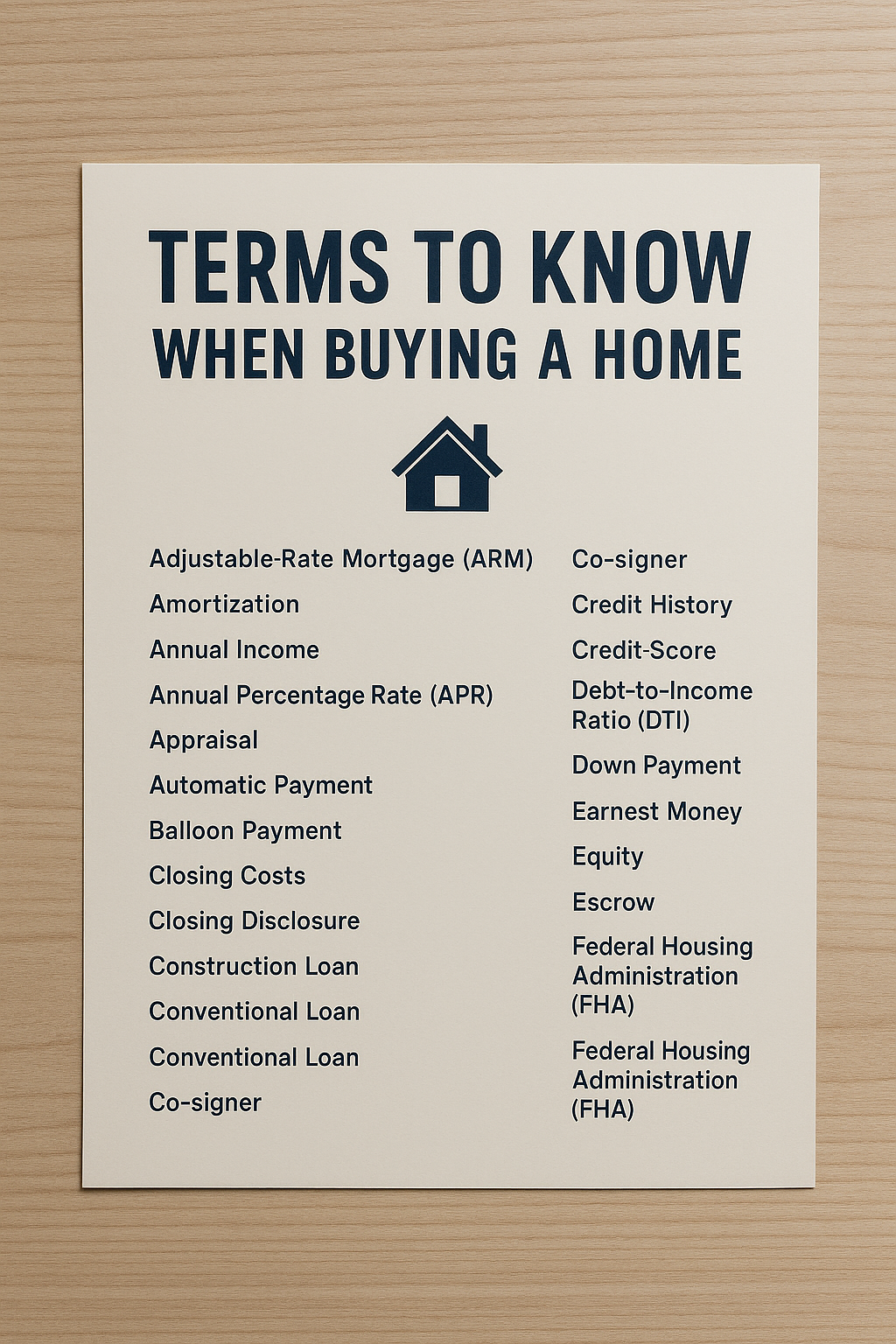

Terms to Know When Buying a Home

Navigating the homebuying process can be overwhelming, especially with all the jargon used. From acronyms in listings to lender-specific terms, it can seem like a different language. Understanding these key mortgage and real estate terms will help you stay confident and informed throughout the entire process.

Adjustable-Rate Mortgage (ARM)

An ARM starts with a fixed interest rate for a set period—typically 5 or 7 years—then adjusts periodically based on market conditions. These loans typically have caps to limit the amount your rate can increase. ARMs can be a smart option if you don’t plan to stay in the home long-term.

Amortization

Amortization refers to the gradual repayment of your loan balance through scheduled monthly payments. A fully amortized loan is paid down to zero by the end of the loan term.

Annual Income

This is your total yearly earnings, including salary, self-employment income, bonuses, tips, and side jobs. Lenders use this to assess how much home you can afford.

Annual Percentage Rate (APR)

APR represents the total cost of your loan, including interest, points, and fees, expressed as a yearly rate. Comparing APRs is the best way to evaluate different mortgage offers.

Appraisal

An appraisal is a third-party estimate of a home’s market value, based on its condition and comparable sales. It’s typically required after your offer is accepted and helps determine loan approval.

Automatic Payment

With auto-pay, your mortgage payment is deducted from your bank account monthly—ensuring on-time payments without the hassle.

Balloon Payment

A balloon payment is a large lump-sum amount due at the end of certain loan types. These loans often have lower monthly payments upfront but require planning for the final payoff.

Closing Costs

Closing costs are the fees required to finalize your home purchase. They usually range from 2% to 5% of the home’s price and cover expenses like lender fees, title searches, and attorney costs.

Closing Disclosure

This federally required document is provided three business days before closing. It outlines your loan terms, fees, and final costs, allowing you to compare it with your original Loan Estimate.

Construction Loan

This is a short-term loan used to finance the building of a home. Construction loans may be issued as one-time-close or two-time-close loans and are available to both builders and owner-builders.

Conventional Loan

A conventional loan isn’t backed by the government and includes fixed-rate and adjustable-rate mortgages. These are among the most common loan types in the U.S.

Co-signer

A co-signer is someone who agrees to take responsibility for the loan if the primary borrower can’t make payments. This can help improve loan approval odds or secure better terms.

Credit History

Your credit history tracks how you’ve managed credit accounts and payments over time. It helps lenders evaluate your reliability as a borrower.

Credit Score

This three-digit number sums up your creditworthiness, based on your credit history. A higher score often leads to better loan terms.

Debt-to-Income Ratio (DTI)

DTI is the percentage of your monthly income that goes toward debt, including your new mortgage. A DTI under 43% is generally required for a Qualified Mortgage.

Down Payment

This is your initial investment toward purchasing a home—usually 20% of the price, though it can be lower with certain loan types. The remainder is covered by your mortgage.

Earnest Money

This deposit (typically 1–2% of the purchase price) shows the seller you're serious. If the sale falls through under certain conditions, the seller may keep this deposit.

Equity

Home equity is the difference between your home’s market value and what you owe on your mortgage. It grows as you pay down your loan or as the property appreciates.

Escrow

Escrow involves a neutral third party holding funds or documents until conditions of the sale are met. It’s also used by lenders to hold money for taxes and insurance.

Federal Housing Administration (FHA)

The FHA insures loans made by approved lenders, making it easier for buyers with low credit or income to qualify for a mortgage.

FHA Loan

This government-backed loan program allows more flexibility for buyers with lower credit scores or smaller down payments.

FHA Mortgage Limits

FHA loans have maximum amounts you can borrow, which vary by location and property type. These limits are updated annually.

First-Time Homebuyers (FTHB)

Typically defined as someone who hasn’t owned a primary residence in the past three years. Many programs offer incentives to FTHBs.

Fixed-Rate Mortgage

With this loan, your interest rate remains the same for the life of the loan—providing stability and predictable payments.

Fannie Mae (FNMA)

This government-sponsored entity buys loans from lenders to ensure mortgage money is available nationwide. Loans must meet Fannie Mae’s standards.

Foreclosure

When a borrower can’t make payments, the lender may seize and sell the home to recover the loan amount. Foreclosures often sell below market value.

Freddie Mac (FHLMC)

Similar to Fannie Mae, Freddie Mac buys mortgages from lenders and sells them as securities. It helps maintain liquidity in the mortgage market.

For Sale by Owner (FSBO)

A home listed for sale directly by the owner without a real estate agent.

Home Equity Conversion Mortgage (HECM)

A reverse mortgage program for homeowners aged 62+, allowing them to borrow against home equity for retirement income.

Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit using your home as collateral. It allows you to draw funds as needed during a set period.

Home Equity Loan (HEL)

This is a lump-sum loan using your home’s equity as collateral. You repay it in fixed monthly installments.

Homeowners Association (HOA)

HOAs manage shared spaces in condos or planned communities. Fees support maintenance and must be factored into your budget.

Homeowner’s Insurance (HOI)

A policy that protects your home and belongings from damage or loss. Required by most lenders before closing.

Inspection

A professional inspection identifies issues with a home's structure or systems. It’s typically done after the offer is accepted and can affect your buying decision.

Index

The index is a benchmark interest rate that reflects market conditions and helps determine the rate on adjustable-rate mortgages.

Interest-Only Loan

You pay only interest for a set period before principal payments begin. This lowers initial payments but increases them later.

Interest Rate

This is the cost of borrowing money, shown as a percentage. Lower rates generally mean lower monthly payments.

Jumbo Loan

A loan that exceeds government-set limits. Often used for luxury properties, they usually have stricter requirements.

Lien

A legal claim on a property by a lender until a debt is repaid. Mortgages are a common form of lien.

Loan Estimate

This 3-page form gives you a breakdown of your potential loan terms and costs. It's issued within 3 business days of your loan application.

Loan-to-Value (LTV) Ratio

LTV compares the loan amount to the property’s value. A lower LTV means less risk for the lender and may lead to better loan terms.

Mortgage Insurance

Insurance that protects the lender if you default. Typically required if your down payment is under 20%.

Mortgage Term

This is the length of time you have to repay your mortgage—commonly 15, 20, or 30 years.

Multiple Listing Service (MLS)

A shared database real estate agents use to post and find home listings. Sites like Zillow pull data from the MLS.

Payoff Amount

The amount needed to completely pay off your mortgage, including principal, interest, and any fees.

Points

Points (or mortgage discount points) are optional fees you can pay upfront to lower your interest rate over time.

Prepayment Penalty

A fee some lenders charge if you pay off your loan early. Be sure to ask if your loan includes one.

Principal, Interest, Taxes and Insurance (PITI)

These four components make up most mortgage payments. Some lenders roll them into one monthly payment.

Private Mortgage Insurance (PMI)

Required if your down payment is below 20%, PMI protects lenders if you default. It can usually be removed once you build enough equity.

Property Taxes

Local governments assess property taxes based on home value. These fund public services like schools and infrastructure.

Purchase Agreement

This is the contract between buyer and seller outlining the terms of the home sale. It becomes binding once signed.

Refinance

Refinancing replaces your current mortgage with a new one—usually to get a better rate, lower payments, or cash out equity.

Servicer

Your loan servicer is the company that manages your mortgage and collects your payments. It may differ from your original lender.

Temporary Buydown

A temporary buydown lowers your mortgage rate for the first year or two—often covered by the seller as an incentive.

Truth In Lending Act (TILA)

A federal law that ensures transparency in lending. It requires lenders to disclose all loan terms and costs to protect borrowers.

TILA RESPA Integrated Disclosures (TRID)

Also known as "Know Before You Owe," this rule merges the TILA and RESPA disclosures into two simplified forms: the Loan Estimate and Closing Disclosure.

USDA Loan

Backed by the U.S. Department of Agriculture, USDA loans offer affordable financing for rural or suburban homebuyers with low or moderate income.

VA Loan

Available to eligible veterans, active-duty military, and their families, VA loans offer low-interest, zero-down-payment mortgages backed by the Department of Veterans Affairs.

Terms to Know When Buying a Home

Navigating the homebuying process can feel overwhelming, especially with all the jargon thrown around. From acronyms in listings to lender-specific terms, it can seem like a different language. Understanding these key mortgage and real estate terms will help you stay confident and informed every step of the way.

Adjustable-Rate Mortgage (ARM)

An ARM starts with a fixed interest rate for a set period—typically 5 or 7 years—then adjusts periodically based on market conditions. These loans usually have caps to limit how much your rate can rise. ARMs can be a smart option if you don’t plan to stay in the home long-term.

Amortization

Amortization refers to the gradual repayment of your loan balance through scheduled monthly payments. A fully amortized loan is paid down to zero by the end of the loan term.

Annual Income

This is your total yearly earnings, including salary, self-employment income, bonuses, tips, and side jobs. Lenders use this to assess how much home you can afford.

Annual Percentage Rate (APR)

APR represents the total cost of your loan, including interest, points, and fees, expressed as a yearly rate. Comparing APRs is the best way to evaluate different mortgage offers.

Appraisal

An appraisal is a third-party estimate of a home’s market value, based on its condition and comparable sales. It’s typically required after your offer is accepted and helps determine loan approval.

Automatic Payment

With auto-pay, your mortgage payment is deducted from your bank account monthly—ensuring on-time payments without the hassle.

Balloon Payment

A balloon payment is a large lump-sum amount due at the end of certain loan types. These loans often have lower monthly payments upfront but require planning for the final payoff.

Closing Costs

Closing costs are the fees required to finalize your home purchase. They usually range from 2% to 5% of the home’s price and cover expenses like lender fees, title searches, and attorney costs.

Closing Disclosure

This federally required document is provided three business days before closing. It outlines your loan terms, fees, and final costs, allowing you to compare it with your original Loan Estimate.

Construction Loan

This is a short-term loan used to finance the building of a home. Construction loans may be issued as one-time-close or two-time-close loans and are available to both builders and owner-builders.

Conventional Loan

A conventional loan isn’t backed by the government and includes fixed-rate and adjustable-rate mortgages. These are among the most common loan types in the U.S.

Co-signer

A co-signer is someone who agrees to take responsibility for the loan if the primary borrower can’t make payments. This can help improve loan approval odds or secure better terms.

Credit History

Your credit history tracks how you’ve managed credit accounts and payments over time. It helps lenders evaluate your reliability as a borrower.

Credit Score

This three-digit number sums up your creditworthiness, based on your credit history. A higher score often leads to better loan terms.

Debt-to-Income Ratio (DTI)

DTI is the percentage of your monthly income that goes toward debt, including your new mortgage. A DTI under 43% is generally required for a Qualified Mortgage.

Down Payment

This is your initial investment toward purchasing a home—usually 20% of the price, though it can be lower with certain loan types. The remainder is covered by your mortgage.

Earnest Money

This deposit (typically 1–2% of the purchase price) shows the seller you're serious. If the sale falls through under certain conditions, the seller may keep this deposit.

Equity

Home equity is the difference between your home’s market value and what you owe on your mortgage. It grows as you pay down your loan or as the property appreciates.

Escrow

Escrow involves a neutral third party holding funds or documents until conditions of the sale are met. It’s also used by lenders to hold money for taxes and insurance.

Federal Housing Administration (FHA)

The FHA insures loans made by approved lenders, making it easier for buyers with low credit or income to qualify for a mortgage.

FHA Loan

This government-backed loan program allows more flexibility for buyers with lower credit scores or smaller down payments.

FHA Mortgage Limits

FHA loans have maximum amounts you can borrow, which vary by location and property type. These limits are updated annually.

First-Time Homebuyers (FTHB)

Typically defined as someone who hasn’t owned a primary residence in the past three years. Many programs offer incentives to FTHBs.

Fixed-Rate Mortgage

With this loan, your interest rate remains the same for the life of the loan—providing stability and predictable payments.

Fannie Mae (FNMA)

This government-sponsored entity buys loans from lenders to ensure mortgage money is available nationwide. Loans must meet Fannie Mae’s standards.

Foreclosure

When a borrower can’t make payments, the lender may seize and sell the home to recover the loan amount. Foreclosures often sell below market value.

Freddie Mac (FHLMC)

Similar to Fannie Mae, Freddie Mac buys mortgages from lenders and sells them as securities. It helps maintain liquidity in the mortgage market.

For Sale by Owner (FSBO)

A home listed for sale directly by the owner without a real estate agent.

Home Equity Conversion Mortgage (HECM)

A reverse mortgage program for homeowners aged 62+, allowing them to borrow against home equity for retirement income.

Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit using your home as collateral. It allows you to draw funds as needed during a set period.

Home Equity Loan (HEL)

This is a lump-sum loan using your home’s equity as collateral. You repay it in fixed monthly installments.

Homeowners Association (HOA)

HOAs manage shared spaces in condos or planned communities. Fees support maintenance and must be factored into your budget.

Homeowner’s Insurance (HOI)

A policy that protects your home and belongings from damage or loss. Required by most lenders before closing.

Inspection

A professional inspection identifies issues with a home's structure or systems. It’s typically done after the offer is accepted and can affect your buying decision.

Index

The index is a benchmark interest rate that reflects market conditions and helps determine the rate on adjustable-rate mortgages.

Interest-Only Loan

You pay only interest for a set period before principal payments begin. This lowers initial payments but increases them later.

Interest Rate

This is the cost of borrowing money, shown as a percentage. Lower rates generally mean lower monthly payments.

Jumbo Loan

A loan that exceeds government-set limits. Often used for luxury properties, they usually have stricter requirements.

Lien

A legal claim on a property by a lender until a debt is repaid. Mortgages are a common form of lien.

Loan Estimate

This 3-page form gives you a breakdown of your potential loan terms and costs. It's issued within 3 business days of your loan application.

Loan-to-Value (LTV) Ratio

LTV compares the loan amount to the property’s value. A lower LTV means less risk for the lender and may lead to better loan terms.

Mortgage Insurance

Insurance that protects the lender if you default. Typically required if your down payment is under 20%.

Mortgage Term

This is the length of time you have to repay your mortgage—commonly 15, 20, or 30 years.

Multiple Listing Service (MLS)

A shared database real estate agents use to post and find home listings. Sites like Zillow pull data from the MLS.

Payoff Amount

The amount needed to completely pay off your mortgage, including principal, interest, and any fees.

Points

Points (or mortgage discount points) are optional fees you can pay upfront to lower your interest rate over time.

Prepayment Penalty

A fee some lenders charge if you pay off your loan early. Be sure to ask if your loan includes one.

Principal, Interest, Taxes and Insurance (PITI)

These four components make up most mortgage payments. Some lenders roll them into one monthly payment.

Private Mortgage Insurance (PMI)

Required if your down payment is below 20%, PMI protects lenders if you default. It can usually be removed once you build enough equity.

Property Taxes

Local governments assess property taxes based on home value. These fund public services like schools and infrastructure.

Purchase Agreement

This is the contract between buyer and seller outlining the terms of the home sale. It becomes binding once signed.

Refinance

Refinancing replaces your current mortgage with a new one—usually to get a better rate, lower payments, or cash out equity.

Servicer

Your loan servicer is the company that manages your mortgage and collects your payments. It may differ from your original lender.

Temporary Buydown

A temporary buydown lowers your mortgage rate for the first year or two—often covered by the seller as an incentive.

Truth In Lending Act (TILA)

A federal law that ensures transparency in lending. It requires lenders to disclose all loan terms and costs to protect borrowers.

TILA RESPA Integrated Disclosures (TRID)

Also known as "Know Before You Owe," this rule merges the TILA and RESPA disclosures into two simplified forms: the Loan Estimate and Closing Disclosure.

USDA Loan

Backed by the U.S. Department of Agriculture, USDA loans offer affordable financing for rural or suburban homebuyers with low or moderate income.

VA Loan

Available to eligible veterans, active-duty military, and their families, VA loans offer low-interest, zero-down-payment mortgages backed by the Department of Veterans Affairs.